Market insight June 14

After yesterday's catastrophic meltdown, normally, I would assume a small pause.

The situation is that the Federal Reserve will announce a new rate on Wednesday, and the market had to readjust its expectations for what the Fed may do in light of the recent CPI report.

Previously, there was a 76% chance that the Fed would raise rates by 50 basis points to a target rate of 125 to 150.

However, the CPI readings shocked the markets, and the market had to readjust its expectations for what the Fed may do in light of the recent CPI report. Previously, there was a 76% chance that the Fed would raise rates by 50 basis points to a target rate of 125 to 150.

However, the market repriced its expectations to a 90% chance that the Fed will raise rates by 75 basis points, and equity markets fell.

The probability is now 97.5% for a 75-basis-point increase with a target range of 150-175.

Now I'm wondering whether the market has already priced in a rate hike of 75 basis points or more as a worst-case scenario...

But what if the market has already priced in the worst-case situation? If the market has already priced in the worst-case scenario, the present market pricing for the interest rate rise of 75bps would be "dovish" compared to the hypothetical 100bps hike that may be priced in.

Therefore, implied volatility might fall as we approach options expiration on Friday. (IV crush)

If you don't know what an IV crush is, I recommend reading the article I wrote about volatility

https://romanornr.medium.com/options-trading-part-5-vega-volatility-risk-ea368b2dfb23

But here's also a video

Central banks' recent interest rate hikes are a direct response to falling consumer expectations.

the beatings will continue until morale improves

Or in other words

The central banks are likely to keep raising rates until consumer confidence improves.

There are various conversations and rumors that the Federal Reserve is attempting to produce a "positive" surprise by increasing rates by "just" 50 basis points, as opposed to the 75-100 basis points discussed.

Psyops theory

The Federal Reserve might be deliberately trying to create a situation where they can "surprise" markets by only raising interest rates by 50 basis points rather than the 75-100 basis points

That could be a cheap way to manipulate markets by creating an artificial sense of expectation and then not delivering on that expectation. Whether or not this is a successful strategy remains to be seen.

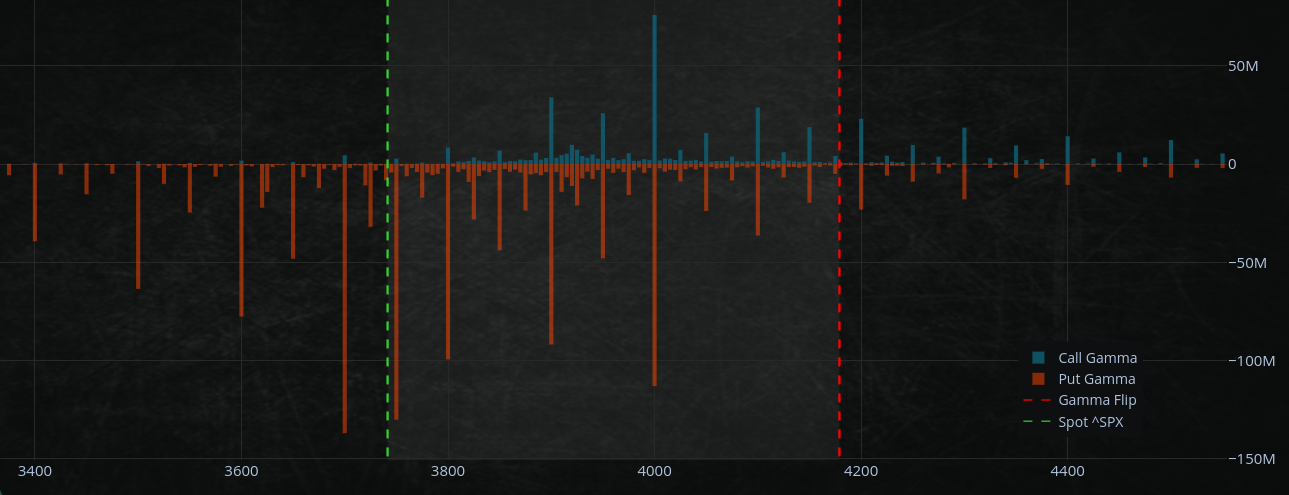

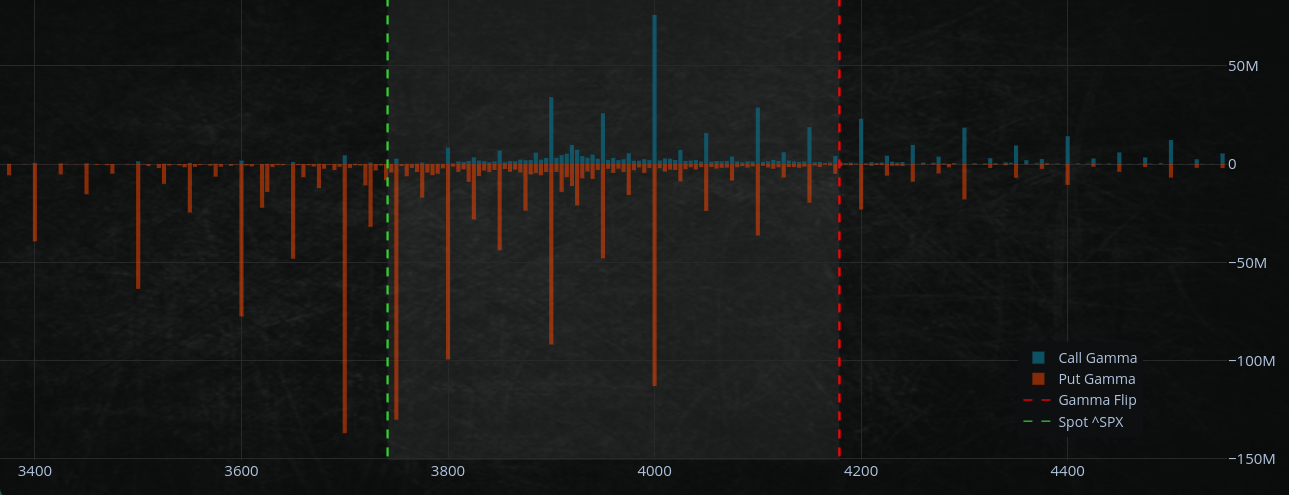

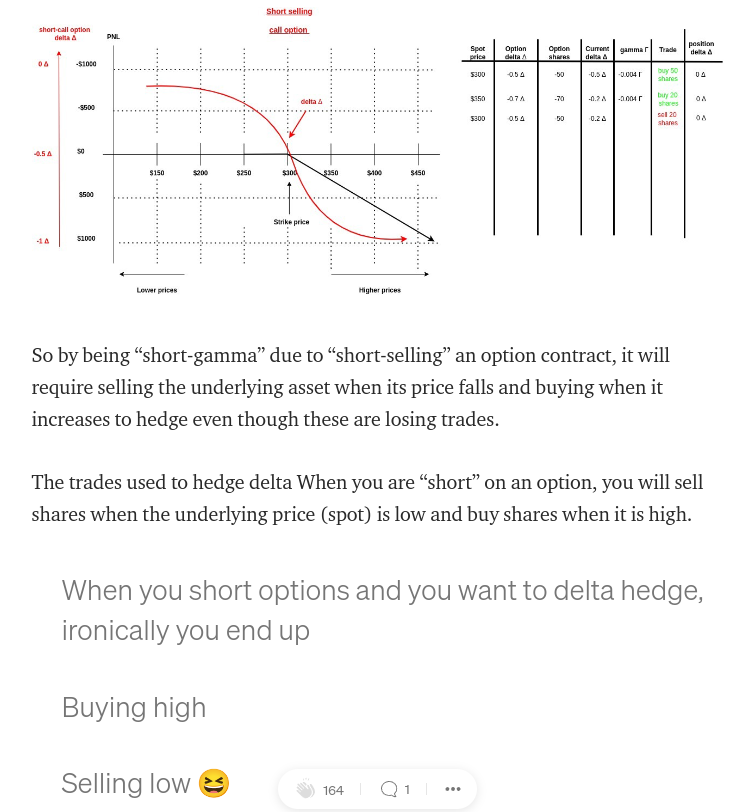

SPX500 option gamma

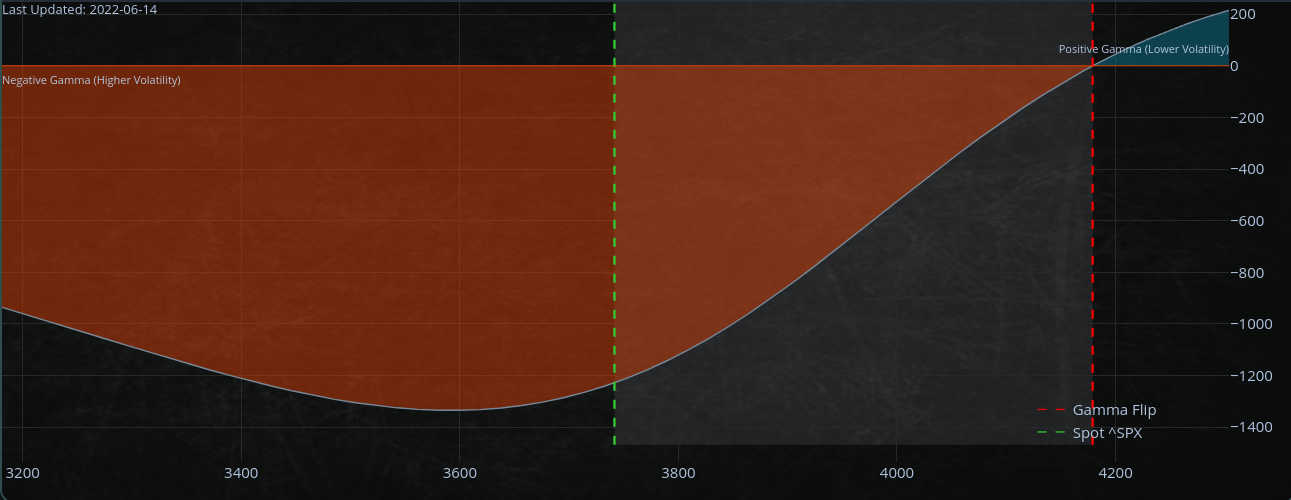

We are still in negative gamma territory on the SPX500

Gamma measures the rate of change of the option price relative to the underlying. Negative gamma indicates that the option price will fall when the underlying asset's price rises. As the underlying price rises, it becomes less probable that the option will be "in the money."

If you want to know more about gamma, I wrote an article about gamma and delta hedging and how that influences a lot of price action.

https://romanornr.medium.com/options-trading-part-3-gamma-curvature-risk-9f6dd4b3db5b

Dealer gamma is the total of the gamma of all options a dealer holds. A negative dealer gamma suggests that the dealer has more options expected to depreciate/decay when the underlying market rises.

That means that intraday volatility will increase since the dealer will need to alter the pricing of the options they hold as the underlying asset price fluctuates.

With the quarterly options expiring in only three days, markets are likely to be sensitive to any changes since many options will expire at this time. That might result in a decline towards the gamma dip around $3600-300 as investors sell options that are unlikely to be valuable at expiry.

Yesterday, in a true negative gamma market fashion, dealers were compelled to chase their deltas, increasing the market's downward pressures. We saw continuous liquidations.

When market participants keep buying "put options" (positive gamma, negative delta), the dealer, on the other will be stuck with the opposite trade, which is "short-put" and therefore has a positive delta and negative gamma.

Prices were falling much more than expected. This forced dealers to hedge their bets and sell the underlying or and futures to get back to delta-neutral, which made the market fall even further. We saw large investors selling their positions while individual investors were not active.

As mentioned in my options article about gamma & delta hedging

https://romanornr.medium.com/options-trading-part-3-gamma-curvature-risk-9f6dd4b3db5b

Screenshot of the article

Continuing, now I get the question a lot:

What is Negative Gamma?

Negative gamma is a measure of convexity. It is the second derivative of the price of an option with respect to the underlying asset/market price. In other words, it measures how the price of the option contract changes as the underlying market price changes.

An option contract with negative gamma ("short-puts, short-calls" and whatever strategy gives a negative gamma exposure.... like FTX MOVE contracts short. Which is basically a short-straddle

Dealers will have to hedge and chase the delta by selling low as the market falls and buying high as the market moves up. Gamma works in both ways.

SPX500 3-Sigma event yesterday

Yesterday, the SPX500 produced a near 3-sigma event as dealers were forced to chase their deltas, exacerbating the market's negative pressures.

You may wonder, what is a 3-Sigma Event?

A 3-sigma event is an event that is three standard deviations from the mean. Standard deviation is a measure of how spread out a set of data is. An event that is three standard deviations from the mean is very rare, happening only 0.27% of the time.

In other words, a 3-sigma event is an event that is very unlikely to happen.

So what happened yesterday?

Yesterday, there was a 3-sigma event in the stock market.

This means that the market fell more than three standard deviations from the mean. This is an infrequent event, happening only 0.27% of the time.

As a result of this event, dealers were forced to chase their deltas.

Delta is a measure of how much the price of an option contract will change in response to a change in the underlying market price.

The market is very "put option" heavy, many people bought puts, and dealers or liquidity providers are stuck with the other side, which is "short-puts", giving them positive gamma exposure, and negative gamma exposure. Dealers were forced to chase their deltas because they were losing money as the market fell.

As the market fell, their positive delta exposure gets bigger and they have to sell the underlying stock/short futures to delta hedge to 0.

That extra pressure on the market, and the market fell even further.

Rumors are there were liquidations of institutional positions. This means that institutions were selling their holdings in the market. (which I didn't confirm or check)

However, that selling put additional pressure on the market, and the market fell even further.

In the days leading up to the Federal Reserve's (FOMC) meeting, the stock market was relatively range-bound.

Key levels on the SPX500 are currently being held at $3700.

The most decisive influence on the options market will be seen after the FOMC meeting and into Friday's expiration of options contracts (OPEX). That is due to the large number of "put options" positions that are to expire on that date which is Friday, June 17.

These positions could create a short-cover relief rally.

OPEX

Okay, so it seems most people don't know what I mean when I tweet about "OPEX," but let me clarify this.

OPEX or OpEx is the Options Expiration Date, the day on which the options contract expires

So there are a lot of put options to expire on the SPX500 at 3600-3700

When a trader buys a put option, they are essentially betting that the underlying market will decrease in value.

If the underlying market declines, the put option will increase in value.

However, if the asset increases in value, the put option will decrease in value.

The amount of exposure to the underlying asset (delta) and the rate of change of that exposure (gamma) will determine how much the put option changes in value.

If the underlying market falls fast with magnitude, the put option will increase in value at a faster rate than if the underlying market decreases in value slowly.

That's because theta, the rate of change of the option's value with respect to time, is small when there is little time to expiry.

Gamma, on the other hand, is large when there is little time to expiry. That is because the option will quickly move from having a lot of intrinsic value to a little intrinsic value when there is little time to expiry.

However, when market participants buy put options, the dealers/market makers/liquidity providers are then stuck with the opposite trade which is a "short-put" exposure, leaving them with positive delta & negative gamma.

They have to hedge since their delta is positive and the market falls, their delta exposure becomes more positive, and their "short-put" position becomes underwater very quickly due to the gamma and convexity. So they have to short-sell futures and or the underlying to hedge their delta back to neutral.

If you have been trading options and delta hedging, you know what I am talking about...

Knowing that liquidity providers are short put options, options deltas decline as expiration approaches, requiring fewer futures/derivs short positions to be held short to balance their books.

When options near expiration, the pressure that has been building up from the "short put" options starts dissipating.

That is because the options' deltas begin to decay, meaning that less of the underlying needs to be sold or futures need short to stay delta neutral to balance their books.

With the expiration of these options, liquidity providers are no longer "short-put" options, and thus no additional selling pressure from them having to delta hedge in negative gamma territory. That buying pressure can help push prices higher after the options expire.